Key Takeaways

- Buying a fixer-upper can be rewarding but requires careful budgeting, thorough evaluation, and strategic planning.

- Understanding the risks and available financing options helps ensure a smoother, more informed home purchase.

Are you considering buying a fixer-upper? This unique real estate path can provide value and customization but comes with important considerations. By following clear steps and understanding potential hurdles, you can approach the process with greater confidence.

What Is a Fixer-Upper Home?

Common Characteristics of Fixer-Uppers

Fixer-uppers are homes that need substantial repairs or renovations before they become fully livable or reach their market potential. These homes often feature outdated systems, aged roofs, worn interiors, or older appliances. Some may require basic cosmetic updates, while others need structural repairs to plumbing, electrical, or the foundation.

Is a Fixer-Upper Right for You?

Ask yourself if you’re prepared for hands-on involvement, both in time and finances. Fixer-uppers are not for everyone—you’ll need patience, flexibility, and a realistic assessment of your skills. If you enjoy DIY projects, have a clear vision, and can manage unexpected issues, a fixer-upper might be a suitable choice.

Why Consider Buying a Fixer-Upper?

Potential Benefits

One major draw is the opportunity to customize a home to fit your needs and tastes. Fixer-uppers often come with lower price tags than move-in ready alternatives. They can provide entry into neighborhoods that might otherwise be out of reach. Renovating also allows you to tailor improvements to your lifestyle.

Possible Drawbacks

Buying a fixer-upper isn’t without risks. Projects can run over budget and timeline. The process can be more stressful, especially if you encounter hidden issues. If you’re not prepared for intensive involvement, or if you have limited resources to cover unexpected costs, a fixer-upper can present real challenges.

What Are the Main Risks Involved?

Repair and Renovation Challenges

Tackling a home in need of work means managing multiple projects—sometimes all at once. Coordinating contractors, getting permits, and sourcing materials can quickly become overwhelming. Some homes might require specialized skills or knowledge to bring them up to code.

Unforeseen Expenses

Unexpected expenses are common in home renovations. Mold, outdated wiring, or foundation issues may not be evident until after purchase. This can add significant costs, so it’s wise to set aside a contingency fund even if your initial inspection looks promising.

Step 1: Assess Your Budget

Estimating Purchase and Repair Costs

Start by determining how much you can comfortably spend, including the home’s purchase price and needed repairs. Obtain several estimates for critical repairs from licensed contractors. Use these figures to build a realistic budget that includes hard costs (labor and materials) and soft costs (permits, fees, and inspections).

Setting Realistic Expectations

Over-optimism is a common pitfall. Prepare for expenses that are likely to come up along the way. It’s helpful to add a buffer of 10–20% over your initial estimates to cover surprises and help keep your project on track.

Step 2: Find Suitable Properties

Using Listings and Local Resources

Begin your search using real estate listings and online databases. Local real estate professionals, community boards, and even word-of-mouth can lead you to hidden gems. Specialty websites may also list homes marked as “fixer-uppers” or “as-is.”

What Should You Look For?

Look for properties in desirable areas where renovations could add value. Pay attention to structural integrity, layout, and location. Prioritize homes needing mainly cosmetic fixes over those with major foundational or system issues unless you’re prepared for a large-scale project.

Step 3: Evaluate Homes Thoroughly

Importance of Home Inspections

Before making an offer, arrange for a professional home inspection. This crucial step uncovers essential repairs and safety concerns. Inspections can reveal issues that may influence your purchase decision and overall project scope.

Identifying Red Flags

Major issues like foundation cracks, outdated electrical systems, or water damage may signal more work and higher costs than expected. If these significant issues arise, weigh whether you have the resources—and desire—to proceed.

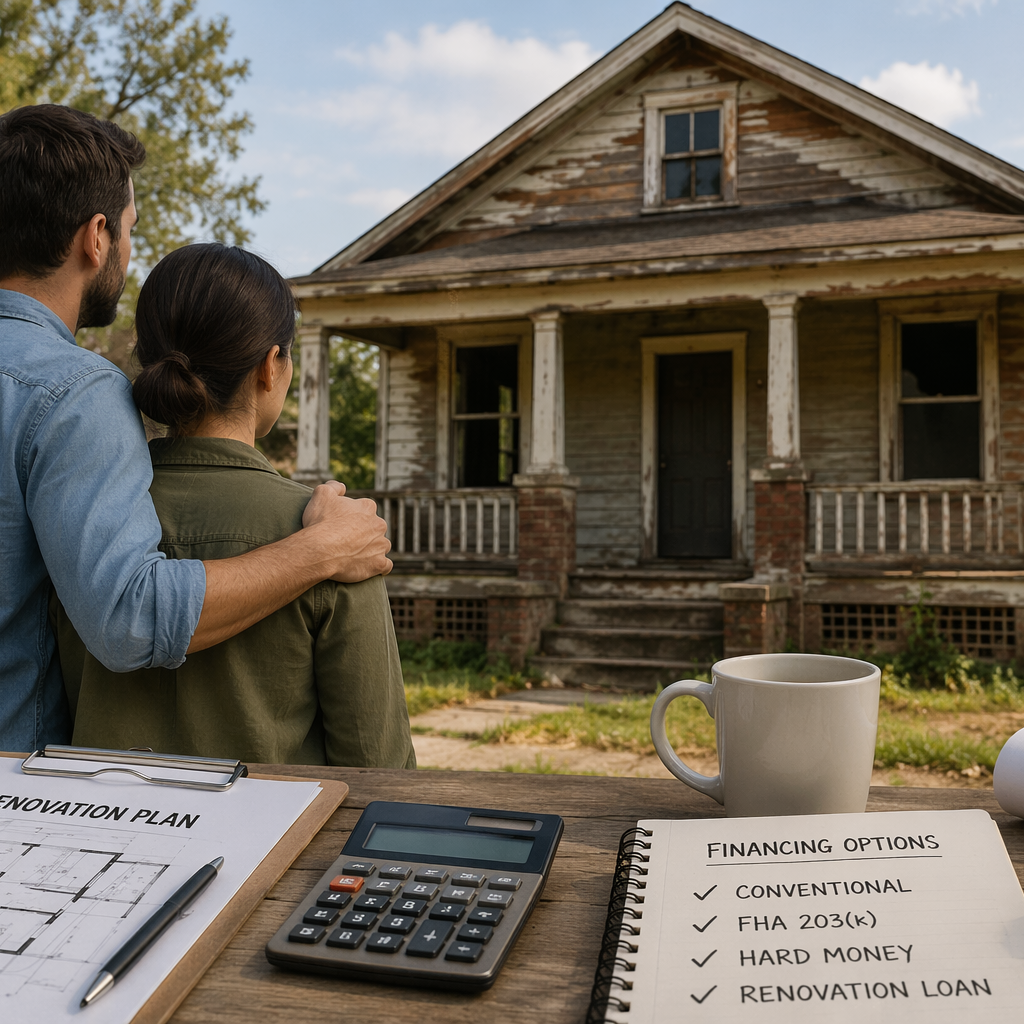

Step 4: Explore Financing Options

Loan Types for Fixer-Uppers

Specialized financing is available for homes in need of renovation. These may include renovation loans, like FHA 203(k) loans or Fannie Mae HomeStyle loans, which wrap the purchase and repair costs into a single loan. Traditional mortgages might apply if the home qualifies, but not all lenders finance properties needing significant repair.

Down Payment and Qualification Basics

Down payment requirements and eligibility vary by loan type and lender. Generally, you’ll need to demonstrate you can afford the combined purchase and renovation costs. Expect to provide income documentation, credit checks, and a detailed renovation plan to support your application.

How Can You Plan Repairs Wisely?

Prioritizing Renovation Projects

List needed repairs from most to least urgent, focusing first on issues affecting safety and functionality—like the roof, plumbing, or electrical systems. Once essentials are addressed, move to cosmetic or optional updates like paint, fixtures, or landscaping.

Building a Realistic Timeline

Create a timeline with input from your contractors. Be sure to accommodate possible delays, including material shortages, permit approvals, or weather changes. A clear timeline keeps your project organized and helps you set expectations.

Step 5: Close on the Property

Understanding the Closing Process

Closing on a fixer-upper is similar to any real estate transaction. You’ll work through escrow, finalize your loan, and complete required paperwork. The process usually takes several weeks from offer acceptance to the official transfer of ownership.

What Documents Will You Need?

Typical closing documents include the sales contract, property disclosures, loan agreement, inspection reports, and renovation plans (if required by your lender). Review each document carefully and ask questions if you need clarity.